How much did they really make on their house?

How much did they really make on their house?

With residential real estate values continuing to soar, everyone has a story about how much money they made on the sale of their house but what are the real numbers?

It’s easy to cheerlead friends, family, and co-workers on the purchase or sale of their home. After all, it is a big purchase and possibly a way for them to notate a change in their lifestyle. We see it all the time:

Wow, double-digit returns on your house in a year! This doesn’t even seem too crazy since the last 5 years have averaged north of 8%.

According to Zillow - The typical home value of homes in North Carolina is $248,950. This value is seasonally adjusted and only includes the middle price tier of homes. North Carolina home values have gone up 15.4% over the past year.

But, what happens when you look at the long-term data and account for those phantom costs?

Down Payment (Opportunity Cost)

Transaction Fees

Maintenance

Interest Expense

Value of your time

These are rarely mentioned when someone is referencing how much money they made from the sale of their home. One of the things that are surprisingly always mentioned? Taxes.

People love to discuss how they took advantage of a 1031 exchange to avoid paying capital gains on their real estate. Conveniently they fail to mention that they didn’t get to experience any benefits of a liquidity event and instead have more real estate.

Or they mention the two-year exemption on their primary residence where they don’t have to pay taxes anymore. Conveniently they fail to mention that they are now paying 6% of the gross sales price in transaction costs which will take a nice bite out of their returns.

We want everyone to make money on all of their purchases, especially their home. Just as importantly, we want their financial plans to follow a data-driven set of repeatable tasks. This will give them the highest possibility of a successful outcome.

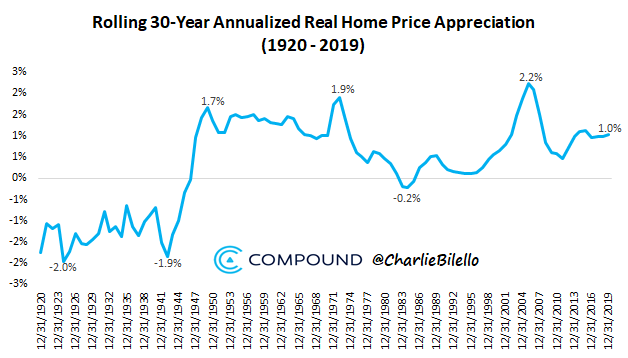

Now, how about those long-term trends? How much money is everyone making? Let’s look at the returns that factor in a 30-year rolling period and inflation.1

Not as exciting when you see returns between -2% and 2%. This is also how we factor in someone’s primary residence to the rest of their investment portfolio. For financial planning purposes, we assume that it will track along with inflation.

When we see clients realize higher returns than this (and we have absolutely seen this) this is a great win and worth celebrating. This can happen with any asset and we want to make sure clients are keeping reasonable expectations no matter where they are in the cycle.

Remember, there are two sides to every trade, you have to be right on both and this typically takes years and the benefit of hindsight to truly realize.

https://compoundadvisors.com/2020/homes-castles-and-price-expectations