Dividend-Paying Stocks have consistently been recognized as a great place to “earn income” outside of your 9-5.

Dividend-Paying Stocks have consistently been recognized as a great place to “earn income” outside of your 9-5.

Make sure that your money is working from you and that your investments are as tax efficient as you are.

This investing style has never made sense to me but there is an industry whose primary goal is to create income from your money. Now, there is some credence in having a well-thought-out systematic withdrawal strategy, knowing which accounts to pull from, and when to make adjustments. This is not what I am talking about.

Usually, this income is generated from expensive, fixed annuity products, but we also see ‘Dividend Aristocrat’ stock portfolios portrayed as the solution to income needs. Here is why I think the only reason to buy such a thing is if you love paying taxes.

Income, especially in retirement, is a sensitive subject. The goal of any working person who has saved, planned, and invested for their retirement is to retire once. So, the idea that your salary is going to turn off forever and you do not know where your next paycheck is going to come from is a fair reason to be concerned. It is also why these income solutions are marketed so boldly.

Have you ever taken money out of your checking account before? That may sound overly simplistic but that is how easy it is to “create” income in retirement. You (hopefully) have saved roughly 20x your annual spending and have a systematic withdrawal strategy where you are comfortable taking out 4% of your nest egg every year.

So why pay taxes when you don’t have to? A dividend is a forced distribution from an investment that you receive and then pay out a percent in income taxes. It does not matter if you reinvest the dividend or take it as cash. You must pay taxes on it. Not just any kind of tax, but generally speaking this is ordinary income, meaning at the percent of your normal tax rate. For high-earning physicians, that is typically the top two tax brackets meaning either 35% or 37% for federal taxes, and tack on another 5.25% if you live in North Carolina.

So when you receive a $100 dividend check you received, $35 goes to Uncle Sam and another $5 goes to the great state of North Carolina.

If you are trying to meet your income requirement in retirement, now all of a sudden, you need to withdraw even more cash to pay your bills. This dividend aristocrat might sound fancy but is really just expensive.

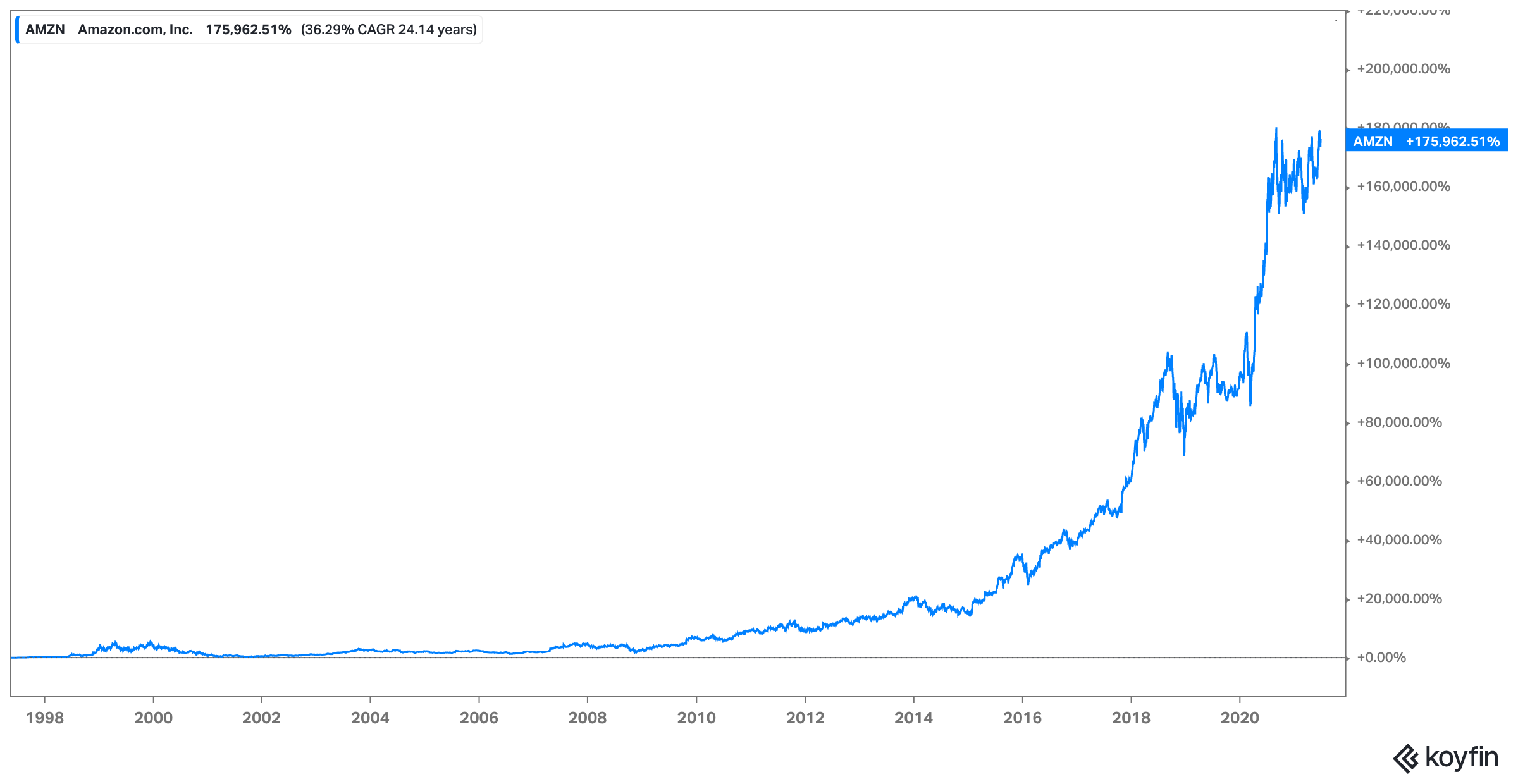

Eventually, everyone is going to draw down their nest egg and that takes some planning, but dividends are not the only solution. Let’s use a real-life example of two amazing investors who invested $250k in their son’s company in 1995 and have not received a single dividend in more than two decades. Now, important to note, they also have not sold a single share of that stock, so they have not had a single tax bill from this investment in over 20 years!

The investors happen to be Jackie and Mike Bezos who bought 1.4 million shares of Amazon stock. This is how it worked for them and then let’s talk about how they may be able to draw income from this portfolio. It is important to note that Jackie and Mike actually invested before the company was public, which means their actual returns are dramatically higher, but that doesn’t change the point.

The best income strategy is having a large investment account and only needing to draw down a small portion at a time. 4% is widely recognized as a safe withdrawal rate and YOU get to choose when you take that money out. The tax code has benefits to being a long-term investor! Instead of the ordinary income tax rate we described earlier, you can be eligible for long-term capital gains which are closer to 20%. Jackie & Mike Bezos will likely be taxed at the 20% long-term rate than the estimated 35% income tax rate. That is almost half the tax rate they would have paid on dividends!

This is an amazing example because Bezos invested in one of the best growth stocks of the century. We do not expect everyone to find the next Amazon to invest in and hold it through many volatile periods, but we certainly hope you do! We can help make sure your investment rules guide your retirement accounts and set a systematic withdrawal rate for your retirement.

Investment Rule: Absolute Returns are what matters. This means the amount of funds that investment has earned. It doesn’t matter if it comes in the form of a dividend or market appreciation. What matters is what you keep in your account at the end of the day.

What’s on your mind?

We’ll be sharing tidbits of wisdom like this with any subscriber every two weeks, along with deeper dives for our clients every month or so.

What questions do you have that we can answer in future posts? Reply directly to this email and let me know.

Talk soon,

Chris

-----------------

Fortress Physicians by the Numbers

🏡 42 Physician Households as Clients

💰 $680,000 Avg Household Income

👩 Average Age 44

💸 $3.25 Million Net Worth

📈 29% Average Savings Rate